On February 21, the stainless steel market remained highly active. The electronic trading of the SS05 contract continued to be vibrant, with intense competition between long and short positions. On the same day, the SS05 contract fluctuated at highs upon opening, reaching the highest price of the day before trending downward. Its subsequent movements were highly uncertain, influenced by a mix of complex factors.

Reviewing this week's stainless steel futures market, the trend was highly volatile, showing a pattern of initial decline followed by a rebound. At the beginning of the week, the market was dominated by cautious sentiment. On February 17, the closing price of stainless steel futures was 13,045 yuan/mt, down 0.15% from the previous day, with a cumulative decline of 0.95% over the past five days. However, in the latter half of the week, the market sentiment shifted dramatically. On February 21, the closing price rose to 13,230 yuan/mt, with a daily increase of 0.38% and a cumulative five-day gain of 1.07%.

The recent price increase was driven by multiple factors. A major nickel pig iron smelter in Indonesia encountered unexpected issues, with the overall project capacity utilisation rate in February at only 30%, and nickel pig iron production is expected to decrease by approximately 10,000 mt in metal content. Meanwhile, Beigang New Materials plans to conduct equipment maintenance and upgrades from March to June, which is expected to impact the production of the 200 series, reducing output by approximately 300,000 mt. These developments injected marginally positive sentiment into the futures market. Additionally, a recovery in macroeconomic sentiment provided further support for the price increase.

In the spot market, stainless steel prices rose overall. Although the price increases varied across different series, they undoubtedly sent positive market signals. Prices for the 300 series stainless steel saw a broad rise, with the prices of 304/2B coil (mill edge and slit edge) in Wuxi and Foshan markets increasing by 25 yuan/mt, and the nationwide average price rising by 30 yuan/mt. Prices for various specifications of the 316L series also increased by 25 yuan/mt. This price rise was partly driven by the positive sentiment from the futures market and partly by the maintenance plans of some stainless steel producers, which altered market supply expectations and supported the price increase.

Prices for the 400 series stainless steel also rose. In the Wuxi market, the price of 430/2B coil increased by 25 yuan/mt, while in the Foshan market, the increase was relatively smaller at 5 yuan/mt. The nationwide average price rose by 10 yuan/mt. Although the price increase was not as significant as that of the 300 series, it still demonstrated the resilience of demand for this series in the market, with prices following the upward market trend.

Currently, although the release of downstream demand remains slow, spot prices have risen under the dual influence of the futures market and changes in supply. However, market participants should remain highly vigilant, closely monitoring subsequent changes in demand and the actual impact of maintenance on supply, to adjust their business strategies flexibly and better respond to market fluctuations.

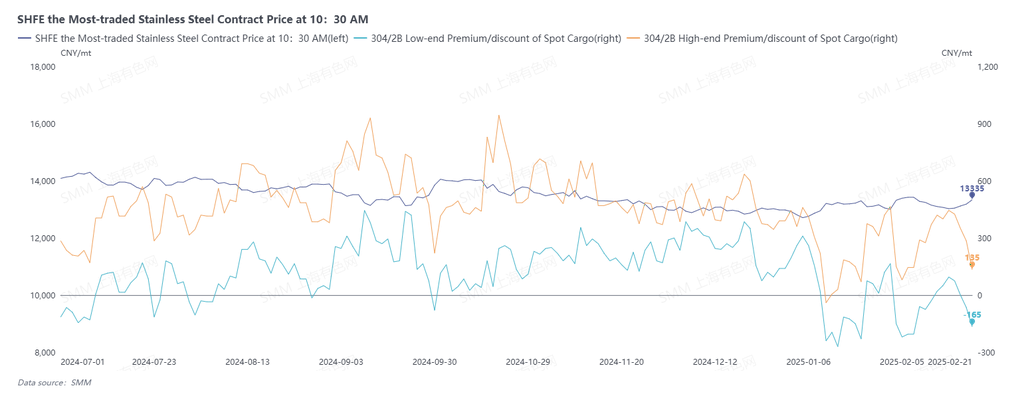

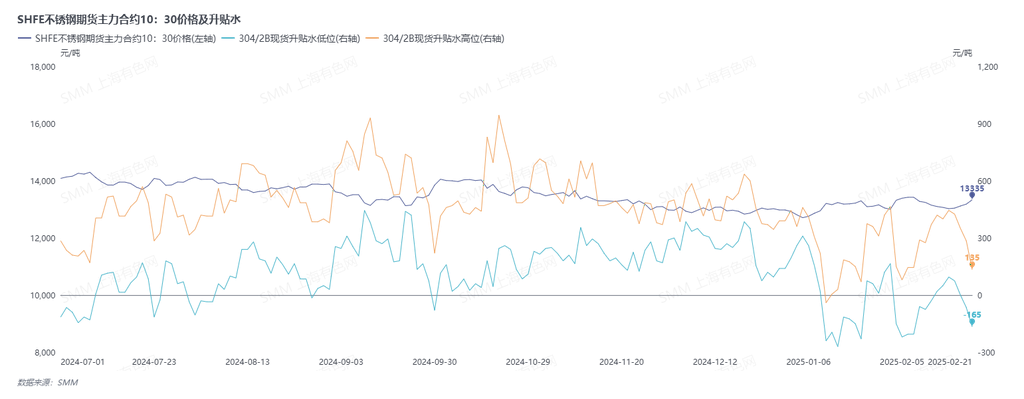

As of 10:30 a.m., the price of the SS2505 contract on the SHFE market was 13,335 yuan/mt. The spot premiums for stainless steel in Wuxi ranged from -165 to -135 yuan/mt. Note: Spot slit edge price = mill edge price + 170 yuan/mt.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)